It's been a strange year in the tech industry. Nvidia (NVDA) invests in OpenAI, which uses that capital to run Nvidia GPUs inside Oracle's cloud. Oracle books growth and orders more Nvidia systems, and the cycle continues.

This is not a meme, it's a capital expenditure (capex) flywheel that converts future AI revenues into today's concrete, steel, and silicon. Uptime and throughput are the play here because compute is the new oil, and these partners own the wells, the pipes, and the refineries.

I explore how the OpenAI–Oracle–Nvidia triangle converts scarcity into a strategy, why it mirrors the Standard Oil and Apple's supply chain strategy, and where the solution will come from if demand, power, or policy abruptly halts the flywheel.

Key Takeaways

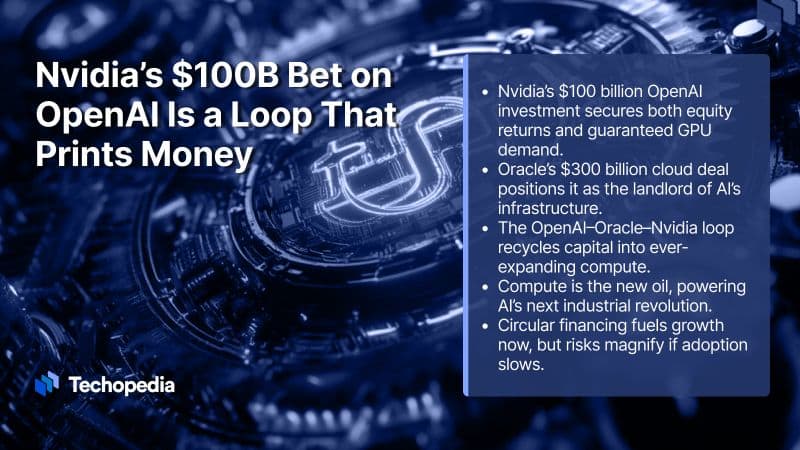

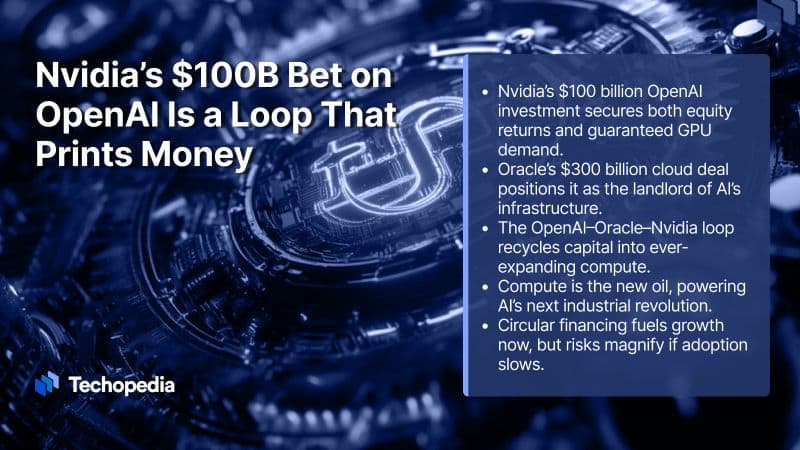

Nvidia's $100 billion OpenAI investment secures both equity returns and guaranteed GPU demand.

Oracle's $300 billion cloud deal positions it as the landlord of AI's infrastructure.

The OpenAI–Oracle–Nvidia loop recycles capital into ever-expanding compute.

Compute is the new oil, powering AI's next industrial revolution.

Circular financing fuels growth now, but risks magnify if adoption slows.

The loop begins: OpenAI and Nvidia lock the flywheel.

Building the Backbone for Endless AI Expansion

A new kind of industrial loop is forming around AI compute. Nvidia has signed a letter of intent to invest up to $100 billion in OpenAI and to supply the startup with data center systems over a multi-year period.

The plan ties capital to capacity milestones, targeting at least 10 gigawatts of Nvidia systems as facilities come online from late 2026.

Crucially, OpenAI is expected to lease most of those GPUs rather than buy them outright, which spreads cash outlays across the useful life of the chips.

In practice, this means that Nvidia becomes both a significant equity investor and the largest supplier of capacity. At the same time, OpenAI secures long-term compute at scale without incurring the full cost on day one.

OpenAI just scored a $100 billion deal with $NVDA Nvidia — but here’s the twist: Nvidia invests in OpenAI, and OpenAI spends that money on Nvidia’s chips.

— Tibo on Tech (@TiboOnTech) September 25, 2025

Circular? Absolutely. $NVDA Nvidia has even done the same with startups like $CRWV CoreWeave and Lambda, renting back its… pic.twitter.com/uv6a27In3j

OpenAI & Nvidia Lock the Flywheel

This is the kernel of the "virtuous cycle" narrative. Equity flows from Nvidia to OpenAI. Orders for compute flow from OpenAI back to Nvidia. The more OpenAI grows revenue for ChatGPT and its enterprise services, the more justification there is for additional capacity, which sustains Nvidia's top line and, by extension, its ability to keep financing the next wave.

Analysts are split. Some call it an efficient way to de-risk a scarce supply chain and make sure the steel gets poured. Others warn about circularity, as Nvidia has been an active investor in dozens of AI companies that also purchase its chips. Both points can be valid at once.

There is also a scale reality that moves this beyond internet hype. Ten gigawatts is the power draw of around ten large nuclear reactors and more than eight million US homes.

You only make commitments like that when you believe real demand is durable. Whether that demand arrives fast enough is the unresolved question.

Oracle, OpenAI & Nvidia Tighten the Circle

Add Oracle, and the flywheel turns faster. Earlier this year, OpenAI signed a five-year, $300 billion cloud contract with Oracle. Markets reacted immediately, with Oracle shares posting their largest single-day surge in decades on the news of record AI bookings and backlog.

The company has since outlined new Stargate sites with OpenAI and SoftBank that push the program toward multiple gigawatts across the US, and is preparing significant bond issues to finance the build.

In that structure, OpenAI's spend flows into Oracle's data centers, Oracle orders Nvidia GPUs at scale, and Nvidia's equity helps OpenAI lease still more capacity. It is not a magic money glitch. It is a capital stack that converts future AI revenue into present infrastructure.

This arrangement also clarifies who carries which risks.

Oracle shoulders real estate, construction, and operations risk for power-hungry campuses.

Nvidia assumes technology and residual value risk through the lease model if depreciation runs faster than expected.

OpenAI accepts product and demand risk. If customers continue to pay for AI services, everyone benefits. If demand slows, leverage and lease obligations bite.

When the Punchline Becomes a Billion-Dollar Strategy

The Three Stooges sketch has been used to describe circular money flows where the same dollar moves through multiple hands, creating the illusion of endless wealth.

It is a funny image, and in the context of Nvidia, OpenAI, and Oracle, the comparison has gone viral. Money flows in, flows out, and ends up back at the starting point, with everyone in the loop looking stronger for it.

But the analogy only goes so far. In the Stooges gag, the dollar never creates anything tangible; it just changes pockets. Here, each turn of the loop results in something that did not exist before: gigawatts of new data centers, racks of GPUs, reinforced grids, and AI services available to customers.

This is why the cycle can look like a comedy sketch on the surface but carry serious weight underneath. The dollars may spin in circles, yet the output – compute capacity – has lasting value.

Like oil refineries or railroads in their day, these assets generate ongoing throughput once built. So while the meme makes for good humor, the reality is a feedback loop that transforms capital into capacity, and capacity into influence.

Nvidia's Playbook for an AI Empire

The oil empire was built by controlling every link in the chain from extraction and transport to refining and distribution. That vertical integration slashed costs and locked in dominance. But it also drew the attention of regulators, who eventually broke up the trust for being too powerful.

The lesson is not just about one company's reach. It is what happens when a platform becomes the choke point for an entire industrial wave. Capital and control fold inward until either regulation or new competitors force the system open again.

Apple offers a modern example. By designing its own chips and locking multi-year manufacturing capacity with TSMC, it gained effective control of supply without owning the fabs. That leverage has become a strategic moat. Nvidia is attempting something similar in the field of AI. It does not run the clouds. It designs the silicon, builds the software stack, orchestrates networking, and now even finances the customers who depend on its hardware.

Compute really is the new oil, only here the rigs depreciate much faster, which means the payoff has to come sooner.

On the opportunity side, this loop compresses time.

Nvidia secures predictable offtake for its following platforms.

OpenAI secures priority access to the rarest input in the tech industry.

Oracle fills its clouds with the highest growth workload on the planet and can justify multi-gigawatt campuses that would otherwise stall.

The triad also reduces coordination friction across chips, software, and facilities, thereby speeding up deployment. When scarcity defines a market, speed creates alpha.

There is also financial elegance. Equity capital from Nvidia de-risks OpenAI's lease profile and improves its ability to raise debt against contracted capacity. Oracle's project finance taps bond markets and spreads risk over decades.

Shareholders in each name see a cleaner story: growth that is not just booked, but physically built. That explains the violent stock reactions around contract disclosures.

AI circle of money ::

— Sam Mielke (@sam_mielke) September 10, 2025

1. $NVDA sells GPUs to $ORCL .. Oracle uses to power its data centers

2. Oracle builds cloud on those GPUs

3. Nvidia rents compute back via signed deals from Oracle

Nvidia gets recurring revenue from hardware sales and cloud services without owning all… pic.twitter.com/2sn679Ao4I

Why Critics Worry

Skeptics see echoes of dot-com vendor financing. Cisco once boosted sales by funding customers who purchased its gear, only to incur losses when the cycle turned.

Nvidia is not making the same loans, but a giant equity stake in a money-losing customer still concentrates risk. If model demand or pricing stumbles, Nvidia could face both slower chip sales and markdowns on its investment. Analysts are already flagging the circular optics and asking whether revenue quality will be clear enough for investors to make informed judgments.

A tighter Nvidia-OpenAI tie could invite scrutiny if rivals argue that the deal hardens barriers to entry at both the chip and model layers. Finally, lease economics assume a useful chip life of up to five years. That assumption will be tested if new architectures shorten the premium window.

Risks Ahead That Matter Most

Demand Risk

OpenAI still needs to pay Oracle at a scale that matches the capacity ramp. If enterprise projects lag or unit costs do not fall fast enough, the loop strains.

CNBC's coverage from Abilene captured the core bet in a single line from OpenAI's CFO: more compute, more revenue. That must keep proving true.

Concentration Risk

A world where one model maker relies heavily on a single chip vendor and one cloud landloper, Nvidia, appears efficient in the upcycle but fragile in a downturn.

It also creates political risk. If policymakers conclude that the loop forecloses rivals, remedies will follow. Reuters has already highlighted potential antitrust attention.

Financing & Balance Sheet Risk

Oracle's new bond programs and Stargate build plans rely on credit markets remaining open and affordable. If rates spike or appetite fades, schedules slip. If they execute, Oracle wins durable tenancy. If not, capex overhangs returns.

Technology Cadence Risk

If alternative accelerators, new interconnects, or more efficient software stacks significantly reduce the cost per token outside Nvidia's roadmap, lease assumptions wobble.

The beauty of the loop lies in its speed. The danger is lock-in.

The Bottom Line

The "infinite AI money glitch" lends itself to a viral frame because it captures a genuine symmetry in how cash, chips, and clouds now feed into one another. The infrastructure being funded is tangible. The strategic positioning is real, and the concern is not a myth either.

Compute is the new oil. The winners will be those who not only pump more of it out but also refine it into something people gladly pay for.

FAQs

What is Nvidia’s $100 billion investment in OpenAI designed to achieve?

Nvidia’s investment secures equity in OpenAI and guarantees long-term demand for its GPUs, fueling AI infrastructure growth while locking in a key customer.

How does Oracle fit into the Nvidia–OpenAI partnership?

Oracle provides the cloud infrastructure for OpenAI’s AI services, purchasing Nvidia GPUs at scale and building massive data centers to support growth.

Why do analysts call this arrangement an AI flywheel?

It’s a self-reinforcing loop where Nvidia funds OpenAI, OpenAI rents Oracle’s cloud, and Oracle buys more Nvidia GPUs, creating continuous expansion.